|

||||||||||||||||

Background

I first became aware that the probity provisions in aged care had been replaced by an approved provider process, in 1999. This was when I sought to object to Sun Healthcare's entry into aged care. The federal Health and Ageing Department had boasted about them in 1993.

My concerns were allayed by an assurance that the Commonwealth was very concerned that "only suitable persons are approved - - - to provide aged care"

In 2006 a Citigroup owned private equity group whose health care operations had already been restricted on probity grounds bought DCA Australia's largest private nursing home owner.

In the probity process the critical determining factor in reaching a decision was "control" as revealed by ownership stake. I learned that control was no longer an issue, unless the management appointed by the controlling owner had a criminal history.

I discovered that any criminal, regardless of their track record could buy an aged care company provided that company already possessed approved provider status. They did not have to seek approved provider status.

Having such status would confer additional value to the company being purchased as a group that might not be considered suitable to operate nursing homes would pay more so be more successful.

After some lobbying I secured undertakings from both the ministers for health and aged care to address the issue but it soon became apparent that this had not happened.

For a detailed account see the web page "Citigroup Buys DCA"

In the meantime the rapid growth of private equity had occasioned some criticism. It seemed to pose a particular risk to health and aged care. In 2007 the Senate Economics Committee held an inquiry into the impact of private equity. I made a submission as did Marie dela Rama et al. Both were discounted by the committee.

In 2007 after only a year, Citigroup sold DCA's nursing home arm, Amity, to BUPA. It was an opportunity to check if any changes had been made. It became apparent that nothing had been done.

In the meantime a new labor government had been elected. They had refused to promise any change before the election.

The new aged care minister was lobbied but refused to address the issue. In 2008 amendments were made to the Aged Care Act 1997. The information released indicated that the amendments would be addressing issues related to the changing nature of financial ownership. I did not believe that the changes would address the issues. I indicated this in a submission to the senate review of the legislation. The bill was passed.

For details of what happened and the correspondence see the web page "Will BUPA seek approved provider status"

To test the legislation a test objection was lodged, in 2009, relating to a company that already owned nursing homes. The department it transpired was not in a position to do anything.

Revelations from Blackstone's 2011 plans

This web page documents issues surrounding Blackstone that emerged when its proposed purchase of the Australian aged care company, Japara, became public.

The Aged Care Crisis Centre drew the attention of the regulator to publicly available material it had acquired. The subsequent correspondence revealed that if Blackstone had proceeded with the purchase

In short there was no protection for the aged - until after they became victims of the system.

On 16th June 2011, The Australian newspaper reported that Blackstone, the giant US private equity group was targeting Japara. It had previously failed in its bid to acquire Australia's second largest health care corporation, Healthscope.

"AFTER more than six months of negotiations, US private equity giant Blackstone is believed to be a week or two away from making a decision on a potential $400 million-plus acquisition of aged-care operator Japara."

Japara operates in Tasmania, Victoria, New South Wales and South Australia. Its has four subsidiaries and runs 35 nursing homes and 5 retirement villages.

Japara had been attempting to sell itself for some time. In September 2010 the Sydney Morning Herald reported that a bitter dispute and court actions involving its sacked CEO was jeopardising the sale prospects. In March 2011 The Age gave further details with one protagonist threatening to have the company wound up.

Although the sale did not eventuate the announcement prompted the Aged Care Crisis Centre to do an internet search. Blackstone was a large US registered Private Equity Group.

The search yielded a cluster of reports surrounding Blackstone's purchase of, first the UK's largest private Nursing Home operator Southern Cross and then the major owner of Southern Cross' leased nursing homes, NHP care homes group.

In 2011 there was intense media discussion as to whether Blackstone, which bought Southern Cross in 2004, had stripped it of assets, and then, in the process of rendering it profitable, tied it into 2.5 per cent rent rises to NHP every year for 35 years. It sold both at a large profit in 2006. Other press comments related to under-investments in resources and to staff being overstretched and on minimum wages.

It was suggested that Southern Cross was left with debts, and a profit margin that could not meet its large ease commitments. As soon as there was a financial downturn it found itself in financial difficulties and unable to meet its debt payments. It had been left vulnerable and with its lease payments locked for 35 years there was little it could do. The care of 31,000 frail elderly was put at risk.

The Guardian newspaper was highly critical of a series of private equity owners.

"Southern Cross's recent problems have followed years of rapid expansion via a business model, which involved the selling off of its freehold properties, and then the company being bought and sold for a whopping profit by other private equity firms.

The effect was to turn it into a billion-pound-plus business, yet the care homes at the heart of it suffered years of under-investment, while staff, many of them toiling for the minimum wage, were stretched to breaking point.

Now union and backbench critics are asking: how did successive governments and regulators allow the provision of social care to be bought and sold like any common or garden commodity?"

The Daily Mail blamed Blackstone

"That deal, while making a fortune for Blackstone���s bosses at the peak of the property boom, saddled Southern Cross with expensive long-term rent commitments it can no longer afford.

The revelation makes a mockery of Blackstone���s claims that it was not involved in asset-stripping the care home operator in the attempt to make a quick profit.

-------------------------

And it admits it was responsible for negotiating the lease deals that left the company committed to 2.5 per cent rent rises every year for 35 years.The inflexible arrangements mean Southern Cross is on the brink of bankruptcy as it struggles to contain its huge �250million rent bill. It reported a pre-tax loss of �311million in the six months to March this year."

The Unions and Southern Cross supported the allegations but Blackstone strongly denied them. It employed a PR firm to counter the damage. Some press and marketplace figures rushed to Blackstone's defence claiming that what they had done was legitimate business.

Further searches were done to see if this was an isolated event. This revealed that

"allegedly siphoning money from the leveraged buyout of Extended Stay America Inc [ESAIN.UL], a deal blamed for the hotel chain's bankruptcy, according to court documents."

Other articles described the flamboyant lifestyle of some of Blackstone's leaders.

All of the allegations were denied by Blackstone.

For more follow the links below.

Australia

- Reuters, 14 May 2010, Healthscope soars on $1.7b buyout offer

- The Sydney Morning Herald, 1 September 2010, CEO departure 'jeopardised Japara sale'

- The Age, 4 March 2011, Bitter feud over Japara

- The Australian, 16 June 2011, Blackstone close to sealing aged-care buy

- The Australian, 5 July 2011, Blackstone still in running for Japara

- Australian Financial Review (Abstracts), 19 July 2011, Blackstone: Japara talks stall

United Kingdom

- Financial Times, 17 September 2004, Blackstone expands with Pounds 162m Southern Cross purchase

- Financial News, 30 November 2004, Blackstone clinches NHP care homes group

- Mail Online, 2nd June 2011, Sharks who made a killing out of 'care': How City predators destroyed firm caring for 31,000 old people

- Guardian, 3 June 2011, Southern Cross care fiasco sheds light on secretive world of private equity

- Daily Mail, 4 June 2011, Revealed: �1bn Gamble Of The Care Home Sharks

- Daily Mail , 16 June 2011, Southern Cross Reprieve After 11th-Hour Rescue Talks

- The Socialist Party, 22 June 2011, Southern Cross bosses demand huge cuts in pay and conditions

- The Wall Street Journal, 4 June 2011, Blackstone Can't Escape Southern Cross Rap

USA

- Reuters, 15 June 2011, Blackstone sued for $8 bln over Extended Stay role

- Mondaq Business Briefing, 28 March 2011, US Second Circuit Restores Securities Class Action Against Global Asset Manager

- Amazonaws.com, 14 June 2011, THE EXTENDED STAY LITIGATION TRUST v THE BLACKSTONE GROUP, L.P.,

- Los Angeles City Attorney, 20 October 2010, Los Angeles City Attorney���s office files legal action against health insurers for defrauding consumers

- The Economic populist, 2011, The Blackstone Group: Tax Fraud Incorporated

- Heinonline, 8 Jul 2010, Taxing Blackstone

- Slate, 3 June 2007, The Golden Ass: How Blackstone CEO Steve Schwarzman's antics may cost him and his colleagues billions of dollars.

- The New Yorker, 11 Feb 2008, The Birthday Party: How Stephen Schwarzman became private equity���s designated villain

Aged Care Crisis Centre was concerned that if there was any substance to these allegations then Blackstone might not be a suitable organisation to control an Australian nursing home company. It felt that Australian authorities should vet the company.

They wrote to the Department of Health and Ageing (DOHA) and copied this to the minister on 8th July 2011 asking if Blackstone had applied for approved provider status.

The Assistant Secretary of the "Prudential and Approved Provider Regulation Branch" replied on 22nd August to the effect that

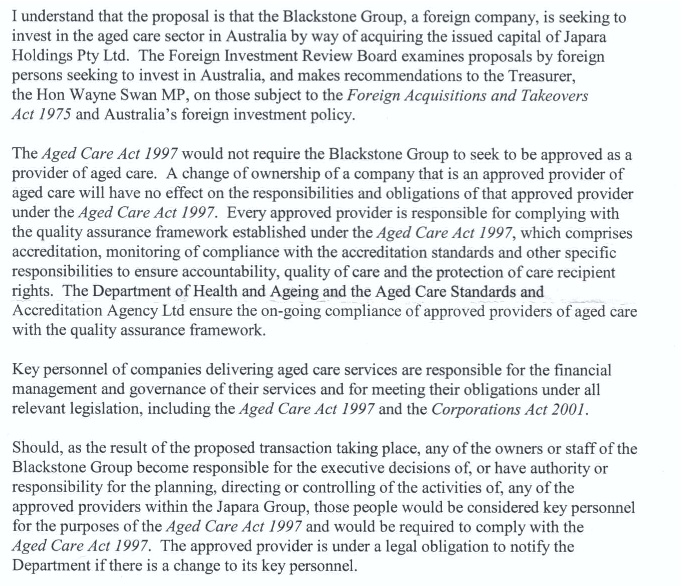

EXTRACT from letter

The letter confirmed that the December 2008 revisions to the Aged Care Act 1997 had not altered the approved provider system to protect our aged care system from unsuitable corporate predators.

Any criminal organisation could buy Australian nursing homes, without any scrutiny, provided the owner they acquired already had approved provided status, provided the managers they appointed to do what they wanted did not have a criminal history, and provided they maintained a minimum level of care sufficient, not to have their homes closed - a recipe for mediocrity.

All shielded by "in confidence" provisions

The letter also revealed that an application for approved provider status is "in confidence". The communities involved, the residents, their families and concerned groups, like the Aged Care Crisis Centre are all excluded. People with relevant information do not know, and the community is locked out and so unable to protest or rock the boat.

Commercial interests are protected over the rights of the community, who will be the customers, and over the interests of the frail elderly trapped in a nursing home now controlled by an operator with a very different agenda. The resident and their family may have chosen with great care, but all that effort was wasted. They might as well have pulled the name out of a hat.

"Choice" is the new mantra from the recent productivity commission report. It seeks to make aged care into a free and "competitive" market. The report completely ignores the loophole in the approved provider process - and the lack of choice for residents, who are the profit bodies sold off for the new owner to exploit.

The system has betrayed the frail elderly and the productivity commission is complicit in this. It has conveniently ignored anything that might make aged care less of a free market.

FIRB does not vet most aged care transactions

The suggestion, in the letter from DOHA, that The FIRB might vet the process was explored.

The Foreign Investment Review Board (FIRB) web site indicates that US companies have special privileges. Except for a few at risk sectors they are only required to seek FIRB's approval when making large investments in companies valued at over $1005 million. For other companies the figure is $231 million. The sensitive health and aged care sectors are not listed among the exceptions.

Few Australian aged care companies would exceed this limit. I sent an email to FIRB in regard to Blackstone to confirm that this was the situation and asked what sort of protection there was for these sectors. I did not get a reply.

It can only be concluded that regulations do not protect the aged care system or the residents from the risks posed by dysfunctional multinational predators. It is also clear that both political parties are so deeply in debt to the providers and their marketplace backers that they will not do anything about it.

|